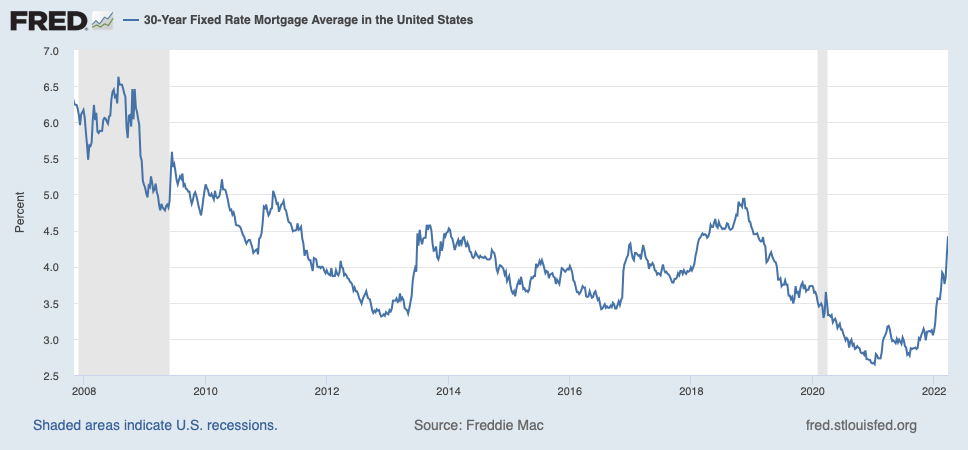

The Treasury yield curve inverted this week. In other words, some shorter-dated Treasury bonds have a higher yield-to-maturity than the longer-dated bonds. This is a highly reliable indicator of recession, although typically the beginning of a recession is still some ways off. Basically, it says that the Fed will raise rates, and then lower them later (because there’s a recession). Normally, this takes place in an environment of a fairly strong economy (that’s why the Fed is raising rates), and the yield curve inversion is brushed off — basically, “this time is different.” Often, the SP500 continues higher for some time afterwards, because of the strong economy. Today, I think the situation is a little different. The Federal Reserve’s rate hikes have everything to do with high CPI figures, or “inflation.” Instead of hiking into a strong economy, it looks like the Fed is hiking into a weak economy, or “stagflation.” In any case, interest rates have been exploding higher across the board, which tends to be bad for business. Here are US 30 year fixed mortgage rates:

I find this a highly risky environment for both stocks and bonds, which is why I continue to emphasize gold and USD cash.

Several people said that they really enjoyed University of Chicago foreign policy expert John Mearsheim’s lecture from 2015, explaining the situation in Ukraine. Here’s a recent followup from Mearsheim and a number of other foreign policy experts.

Doomberg looks at where agricultural production and food prices are headed. As you might imagine, this presentation has a tinge of “doom.” I don’t think anyone in the developed world will go hungry. A more likely outcome, even if world grain production is seriously impaired, is that a substantial amount of grain now directed at animal feed (about 40% of world grain production) will instead be consumed directly. Livestock operators, finding feed too expensive, would cull their herds. But, this would take a major change in behavior, and prices often have to rise a lot before people reduce their driving, turn down their thermostats, or reduce their meat consumption. Look at natural gas in Europe. In other words, agriculture prices might head a lot higher. This would likely be very disruptive in much of the developing world, where incomes won’t keep up with rising food costs. This is more of an economic problem than one of agriculture — the food exists, but it is being fed to pigs and cows. Nevertheless, unrest and even changes in government can follow. There aren’t a lot of equities that are directly tied to farming and farmland, as opposed to farming inputs or middlemen such as fertilizer producers (MOS), equipment producers (DE), or food processors (BG). My short list includes: Gladstone Land (LAND), Farmland Partners (FPI), BrasilAgro (LND), Cresud (CRESY), and Adecoagro (AGRO). The “price of wheat in gold” tells me that, if a real squeeze is upon us, wheat/gold could easily double; and if it got serious, I think 4x higher is plausible (about 2.0 on this chart). That would be about $0.70/pound wholesale price of wheat, which still doesn’t seem too high to me.

The Invesco DB Agriculture Fund (DBA) provides exposure to agricultural futures. These futures-based ETFs are somewhat problematic, but it might be an effective way to gain direct exposure to the commodities, rather than a stock.

On my economics website, I look into how Russia’s central bank could link the ruble to gold at 5000 rubles/gram — which it appears the CBR is actually doing. Amazing!

Thank you Nathan. Looks like we may see a market dip.